Its sad seeing what the US government has become. Not only have they embarked on horrible long term fiscal policy. But they've also created a market that makes it harder to trade bonds. It eliminates a liquid, versatile weapon available in the trading arsenal. The long bond trade. Bonds used to have an asymmetric payoff profile. The downside was limited, because inflation was contained, but the upside was more open ended due to recession risk and an overactive Fed. That asymmetric payoff is now gone. The payoff profile is now more balanced, with inflation risk now just as high, if not even higher than recession risk. Add to that the poor supply/demand fundamentals in the Treasury market with lots of supply coming from the huge deficits and less demand coming from creditor nations like China.

2020 created a sea change in the bond market. With the enormous Covid fiscal stimulus in 2020 and 2021, the fiscal budget blew out and inflation came roaring back. At first, bond traders couldn't believe what was happening, and remained skeptical about the ability for the US economy to stay strong with high interest rates. That's why the SOFR curve has continuously priced in many more rate cuts than have actually happened. Its why the yield curve was so inverted, and remained that way for so long. Its because the majority of bond investors expected the Fed to normalize rates (cutting them to neutral) much more quickly than they have.

Of course, the rate cuts this fall, which have come much later than many expected, are too little too late for bond investors. To add insult to injury, you have seen the biggest 10 year yield increase ever following the first rate cut of the cycle. Its been hell for bond investors for the last 3 years. It is the exact opposite of how bond investors felt for the 10 years prior to 2021. Instead of having both positive carry (upsloping yield curve) and yields trending lower, you have negative carry (inverted yield curve) and yields trending higher. A bearish double whammy. Levered longs in the bond market have gotten killed.

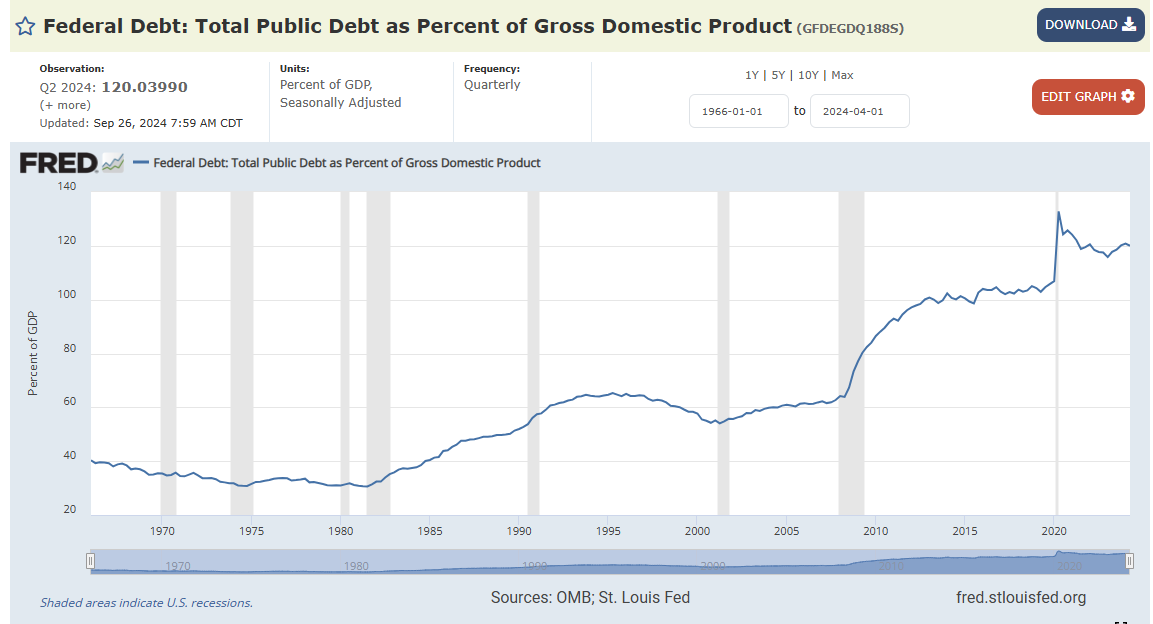

The golden days for the bond investor are over. The cat is out of the bag. There is no turning back when you embark on permanently high fiscal deficits to keep the economy out of recession. It is no longer politically or monetarily feasible to get back to low fiscal deficits with this amount of national debt. The interest on the debt itself is so enormous that its a vicious cycle of issuing more debt to pay the interest on the current debt. Its a national debt treadmill to hell. If the US government even starts on a lower deficit trajectory, it would crush the stock market and the economy so fast that they would quit right after they started.

The US government is acting like KKR. They are acting like the Carlyle Group. They are levering up via Treasury issuance to funnel liquidity to the top 5% in the country, which the top 5% are using to buy large cap US stocks. The public balance sheet gets worse and worse, loaded to the gills in debt, and the private balance sheets gets better and better, loaded up with financial assets. There is no magic to the US economy. Its the US government acting like private equity, using debt to indirectly buy up US stocks through the liquidity that they pour to the rich. Sacrificing the bond market to boost the stock market. It creates the illusion of a strong economy, but its all a money illusion created by nominal growth, which is almost all inflation.

This bond market fragility makes this aging bull market in US stocks so precarious. Stocks and bonds are linked. Investors demand higher equity returns when bond yields are high. Otherwise, investors would rather just invest in the less risky asset with the higher yields. To get higher equity returns, valuations have to be lower. That is why most of the worst selloffs in the post 2008 era have happened after bond yields were rising: August 2011 (European sovereign yields rising), August 2015 (the first Fed rate hike since ZIRP, causing bond yields to rise ahead of the rate hike), October-December 2018 (a rate hike every other quarter for several quarters with 10 year yields rising from 1.32% to 3.24% over 2+ years), and January 2022-October 2022 (most rapid rate hiking cycle in recent history).

The bond market weakness is not an immediate concern, when risk appetite is so hot and heavy like it is now. But it will matter when this rally cools off and the Trump euphoria wears off. I suspect that will happen early next year, as Trump enters office and the reality is less than what it was hyped up to be.

We finally got some liquidation of long positions among asset managers in SPX futures ahead of the election, as shown by the COT data as of last Tuesday, Nov. 5. The absolute net long level is still quite high, but off of the very high net long levels reached in October. That was part of the reason that the risk on rally was so strong last week, as asset managers scrambled to re-add risk, while dealers had to delta hedge their short put positions by covering shorts, as the IVs got crushed, taking the OTM put deltas down with it.

This bid is spilling over into the new week, as we are getting a gap up and enthusiasm is rampant. Bitcoin is over 82K, TSLA is mooning, and speculators are out in force pushing things higher. It is too early to try to be cute and short this monster. This is a freight train that is running over the knee jerk contrarians. Sold part of my SPX long position, but still long some to ride the Trump hype train. Will look to sell the remainder of longs this week if we get a further rally into November opex. Not thinking about fading this train until late November/early December, after more chasers have gotten on board. For the remainder of this month, I would rather short a counter trend bounce in Treasuries than a further rally in stocks. Its a tough time to try to short in November and December, with so many capital gains in stocks that will likely be delayed into 2025. For those with bearish thoughts, or natural born faders, its a good time to take a 2 week break.

8 comments:

You are right. SPX turns weak at around 6000.

do you think S&P could by 7k end of 2025? and Possibly 10-12k end of 2028? They have to inflate away to get out of indebtedness eventually and this may lead to great nominal returns (they can keep changing cpi calculation to show a good number)

Unlikely that S&P will go that high within the next few years. You need a recession for the money spigots to go full blast again, and that's only going to happen AFTER the stock market is already much lower. The US economy is so financialized and dependent on asset price growth, that the only way you get a recession is with a bear market in stocks. Then, if they go batshit crazy with stimmies like they did in 2020 and 2021, then you can get 10K by end of 2028. Its not likely, but its possible.

cool thanks

Seems they want to fire half

The federal workers. That cant be good for the economy and doubt unemployment benefits go up in this administration. May be notjing will break after all

Lots of bluster. Don't believe the hype. They will do what's easy (tax cuts) and threaten to do what's hard (painful tariffs, deportations, cutting spending) but no do them. That's what happened last time Trump was in office. Expecting the same again. Trump will fold like a lawn chair as soon as the SPX goes down 10% on bearish political news.

Is there any chance of stock market being down in any year if trump presidency? He will not like it and he cares a lot so will do anything. Probably not supposed to short anything for next year at least

Trump doesn't control the stock market. He needs Congress to pass any major legislation which is the only way that he can print enough money to pump up the stock market at will. Unless there is a recession, in which stocks are already down big, he's not going to get enough votes to pass a big stimulus bill. Don't think he really cares as much about the stock market as investors believe.

Post a Comment