We are approaching the top of the mountain. For anyone who's climbed a big mountain, the closer you get to the top, the greater the sense of excitement, achievement, and euphoria. This is what is happening in the US stock market. You can sense it from the return of complacency (TACO trade), speculation in risky assets like bitcoin, and even seeing the beginning of a move towards low quality, like the Russell 2000 (massively outperforming SPX in the premarket).

With Russell 2000 lagging so badly over the past year, when it starts outperforming after an extended rally, its often a sign of investor exuberance and excessive speculation. The Russell 2000 is a different barometer than it was in the pre 2020 era. Before 2020, the Russell 2000 usually outperformed coming out of bottoms as risk seeking investors flocked towards the more speculative and higher beta small caps. Back then, Russell 2000 would top out before the SPX and Nasdaq, acting as a canary in the coalmine signal of waning upward momentum. No longer. Now Russell 2000 outperformance is a sign of investor complacency and exuberance, happening after extended rallies.

Tops take time to form, which make them tricky to trade. Tops breed complacency. Bottoms breed fear. The tops that lead to bear markets (not just corrections) usually have the following attributes:

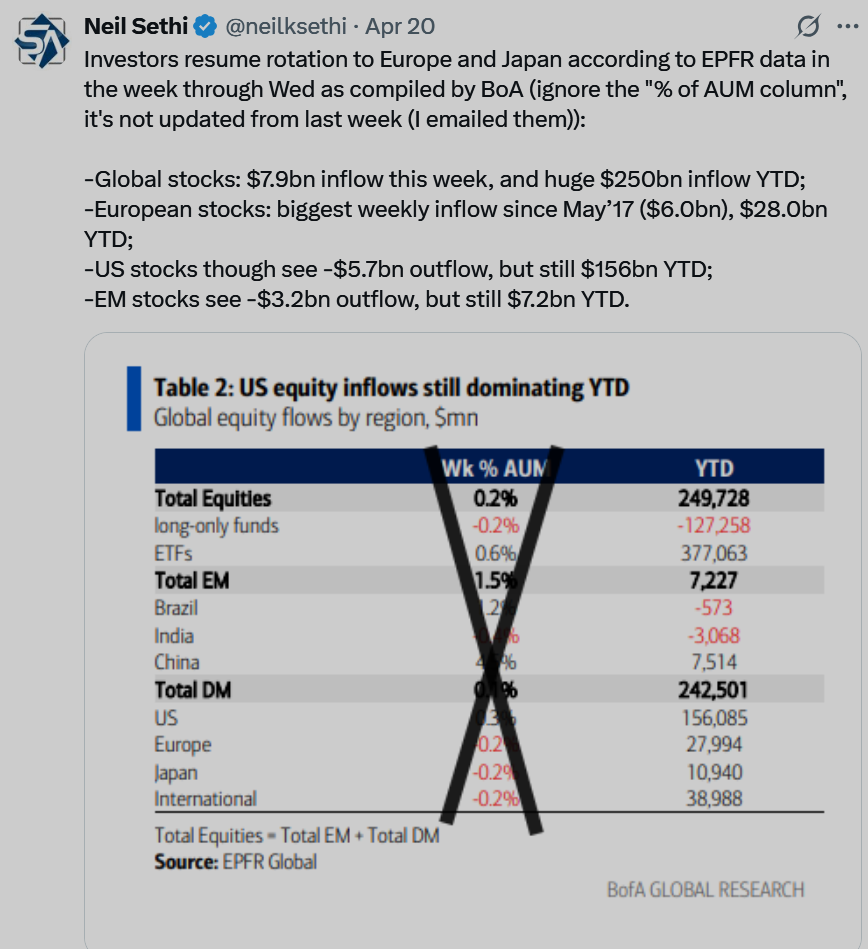

1. Consistently high inflows into equity funds/ETFs and speculative high beta stocks showing increased retail investor interest in stock speculation/investing. (Check)

2. Big gains in the stock indices over the past 2-3 years. (Check)

3. Historically high valuations. (Check)

4 Economic growth decelerating. (Check)

5. Investors getting less bullish as uptrend flattens out and gets choppy, but still staying fully invested. (Check)

We reached a peak in investor bullish sentiment in December 2024, after Trump winning the election. There was euphoria over future tax cuts and deregulation and hopes for a repeat of the SPX performance during Trump's first term from 2016 to 2020. The Fed meeting last December where dove Powell left the room and hawk Powell returned was the beginning of the topping phase. The SPX reached higher highs in February, but investors were getting less bullish as tariff news started to come out. Usually bullish sentiment tops out before prices do. There is often a delay of several months before dropping bullish sentiment eventually shows up in the SPX with a big selloff.

In the 2000 top, investor bullish sentiment actually hit a peak in December 1999, when the original dotcom bubble bellwethers YHOO and AMZN peaked. The Nasdaq continued to go higher until March 2000 but that was led by second wave of dotcom bubble stocks like CSCO, various semiconductors, and speculative biotechs. Just as NVDA was the first wave speculative leader of the 2023-2024 boom due to AI, it topped out before the second wave of more speculative stocks like quantum computing, PLTR/APP type of pseudo AI names, and of course bitcoin, which are still going.

You are seeing a second wave in the bitcoin froth with various junk small caps starting bitcoin treasuries, leading to one day jumps in their stock of hundreds of percent (SBET, NAKA, etc.). We are finally getting some big IPOs in the bitcoin sector, with CRCL and STRD. This is all happening as the US economy is noticeably slowing, with historically nosebleed valuations.

Tops take time, but they don't last forever. The most extended top was in 2000, when the SPX chopped violently in a range for 8 months from December 1999 to August 2000. Then the bear market started in earnest in September. In 2007, the SPX went most sideways from June to October, so 4 months in a choppy range before the start of the bear market. In 2021-2022, the SPX went mostly sideways from September 2021 to March 2022, about 7 months trading in a choppy range before the bottom fell out and the bear market really got started. So the 3 most significant tops in the past 25 years took approximately 4, 7, and 8 months to complete before a bear market really got started.

The SPX is no longer in a clear uptrend, but in a sideways chop, with long term moving averages flattening out. It has been 6 months since bullishness hit a peak last December, and we've been in a choppy range ever since. Given how much time we've gone sideways, something has to give. If my thesis is correct and the current market is forming a meaningful top, history says that there is not much time left before a bear market starts in earnest.

Given that its been 2 months since the SPX bottomed in April, enough time has elapsed for many traders to get back to previous net long exposures. Retail investors have consistently been the most bullish on this market. That is 2000 type of stuff. That is a bad long term sign, as they are historically even worse market timers than the institutions. The TACO trade, less fear about tariffs, more calls for all time highs, and increased complacency among investors are signs that the market has priced in a lot of good news and optimism. It took some time, but hedge fund net flows are now back to beginning of the year levels, and above levels seen at the all time highs in mid February. There is now ammo for both retail and hedgies to panic if we see a significant correction in Q3, which is my base case.

Private client equity allocations at Bank of America show historically high levels. Only the crazy speculative period in 2021 tops the current levels at 63%. This is potential fuel for a nasty bear market if private clients just get back to just average levels of 56%.

The latest COT data was a mixed bag, as asset managers meaningfully decreased SPX long positions even though the market went higher for the week ending June 3. However, small speculators increased their long positions.

You saw something similar as asset managers decreased SPX long positions as the SPX grinded higher in late 2021, as the SPX was making a meaningful top.

Last week was brimming with weak economic data, which was mostly shrugged off. The feared nonfarm payrolls report is behind us, and tariff fears are much diminished with Trump recently having a good call with Xi, opening the door for chicken little longs to buy as there is now more "certainty". Now expectations on tariffs are too bullish, as most assume the drama is over. While that's possible, knowing Trump, he loves to shake the tree to become the center of attention again and then be the one to play hero and make trade deals, pause tariffs, or try to pump stocks by saying its a good time to buy, etc. He is both the arsonist and the firefighter. All the while being the center of attention, which he craves. I expect him to throw a wrench into the TACO trade before the July 9 deadline for the tariff pause. With the amount of buying and re-risking that's happened over the past 2 months, I expect a sharp correction for the next 2-3 months.

Still not yet at that exquisite short moment, but we are getting close enough that I would rather be a bit early than try to time the top perfectly and miss this golden shorting opportunity. Thinking the most likely scenario is a top around SPX 6050 after the CPI release and a short term pop in both stocks and bonds on that data point. But I'll probably start scaling into shorts into any strength this week starting on Tuesday and adding till the end of the week. For those with a bearish bias, this week will be the time to strike.