We are seeing a new pattern that investors are not used to. Ever since 2008, coming out of the financial crisis, the US equity market has continuously outperformed other countries and by a large margin. That has drastically changed in the past 6 weeks. Since the start of April, the US has been a huge laggard.

|

| DAX vs SPX 2022 |

|

| Nikkei 225 vs SPX 2022 |

|

| Shanghai Composite vs SPX 2022 |

|

| MSCI Brazil ETF vs SPX 2022 |

We have finally made the turn, and the market has done its job. It has created the most liquidity and volume for US stocks at the top for US outperformance, which now looks to be 2021. That is a 13 year window of outperformance for US stocks that ended with a blowoff top of epic proportions, as everyone across the globe herded into big cap tech (AAPL, AMZN, MSFT, GOOG, FB, NFLX, TSLA, NVDA, etc.) or into the big 2 US indices: S&P 500 / Nasdaq 100. Those have now become the worst performers, as the underperformance has accelerated over the past 6 weeks.

There are fundamental headwinds for US stocks which weren't present in the last 13 years. We're now in a structurally higher inflation environment with tight commodities markets keeping goods prices high and a massive federal budget deficits which keeps demand artificially high while also keeping money supply growth high. Labor markets are tighter as immigration has trended lower in the US and population has gotten older. This keeps wages higher and gives workers more bargaining power than at anytime in the last 13 years. Higher wages = lower profit margins. Higher inflation = less dovish Fed. I am not a believer that they will try to kill inflation with big rate hikes and very tight policy. They will cave in as soon as the economy slows down enough for people to start complaining about high interest rates and lower stocks. However, they will have a hard time going to QE and rationalizing easy money policies if rents, food, and energy prices keep going higher.

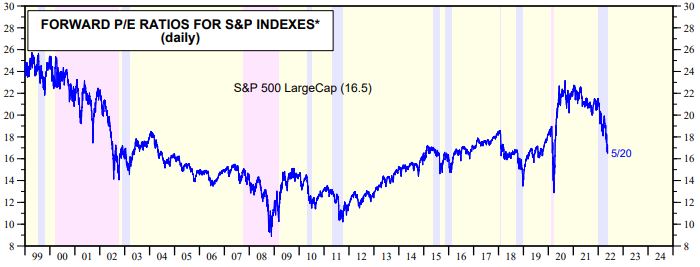

Without QE, I don't see a sustained uptrend in the SPX until all the froth is gone, which would be around the SPX 3000 level. At SPX 3900, the forward P/E is 16.5.

The SPX bottomed at a forward P/E of 14 in 2002, at a forward P/E of under 9 in 2008, under 11 in 2011, and under 14 in 2018. A drop in the forward P/E to 14 would take the SPX to 3300. That is assuming that foward earnings remain the same. But forward earnings estimates seem wildly optimistic, so even a 10% drop in earnings, which seems reasonable considering the slowing economy and falling profit margins, would require the SPX to get down to 3000 to reach a forward P/E of 14. And I haven't even gotten to the worst case scenario of a 2008 or 2011 situation, where forwards P/Es got down to 9 and 11, respectively.

So while many market participants seem to now agree that we are in a bear market, many are still looking for a bounce as the markets look like they are oversold. The trend is down, as the US underperformance and post bubble dynamics reveal. Its hard to make money going long the SPX in that environment. When the market gives you this many changes to go long near the lows, its a sign of weakness. Rarely in the past 13 years did the market offer so many chances to buy the lows as this one has.

Sold the short term long SPX trade for a small gain on Friday, still have a small legacy SPX long left which I will look to sell on a bounce. Still waiting for that elusive and fleeting short opportunity in NDX.

No comments:

Post a Comment