AMZN and GOOG brought out the cherry bombs to the bull parade in after hours. And Europe, as it has a tendency to do, exacerbated the selling and turned it into a panic. The volatility has been through the roof this week. Usually that is a sign of capitulation, and while yesterday's price action before the earnings announcement looked constructive, the investors are nervous and are selling first and asking questions later. In the overnight session, the selling got emotional, and we are retesting those lows made near the Wednesday close.

Based on past experience, usually these emotional gap downs get bought as soon as the US cash market opens. Especially when it has come after several days of selling. I expect there to be buying when the US regular cash session opens. Long term, these negative earnings reactions to relatively benign earnings from AMZN and GOOG do tell you that the leadership is no longer outperforming, and that means the bull market is basically over. But even if its a bear market now, I expect there to be an oversold bounce that lasts at least 2 weeks going into a positive seasonal period.

Friday, October 26, 2018

Thursday, October 25, 2018

Shades of 2000 and 2007

This is the beginning of the end of the 10 year bull market. I made a tactical error treating this like just an ordinary correction in a bull market, expecting buyers to be there when the market got panicky, but clearly without the stock buybacks (blackout will be lifted for most companies starting next week), there is no support for this market. All the leading indicators showing a slowing economy in 2019, with the Fed still unwilling to stop their hiking path without bigger weakness in the stock market, means the Fed put will not be the support that it used to be. The Fed put strike price is much lower than current SPX levels.

I believe we are topping out here much like in 2000 and 2007. The initial sharp selloff in 2000 occurred in April, and then it was lights out in October. In 2007, the initial sharp drop was in late February, followed by a big, scary dip in August 2007, and then it went down in earnest starting in November. 2018 had the big scary dip in February with retest in April, and now another big drop in October. This feels more like August 2007 than October 2000, so there should be a sharp rally in November. If not, the rally should only last 2-3 weeks and then go back down again. Considering the seasonal tailwinds, I expect a 4-6 week rally towards at least 2870.

SPX 2000

SPX 2007

SPX 2018

Now that I am stuck in a pickle, buying the dip, I will try to wriggle my way out of this mess. There is no way this gap up will be sustainable going into the middle of the US cash session, so I expect sellers to immediately bring down this gap up at 2684,as I am writing, when the US cash market opens. There should be initial support at SPX 2660, and yesterday's lows at 2652. I would wait till after Europe closes, during the US lunch hour to think about buying a dip. If the SPX is below 2660 at that point, it could be a good dip buy looking for an oversold intraday reversal. I hate to do it, but I will need to do some microtrading intraday to try to pick up some points from the bad long entries last week and earlier this week.

There should be a decent intraday bounce coming up after this week is finished, as the stock buybacks will be back with a vengeance starting next week.

I believe we are topping out here much like in 2000 and 2007. The initial sharp selloff in 2000 occurred in April, and then it was lights out in October. In 2007, the initial sharp drop was in late February, followed by a big, scary dip in August 2007, and then it went down in earnest starting in November. 2018 had the big scary dip in February with retest in April, and now another big drop in October. This feels more like August 2007 than October 2000, so there should be a sharp rally in November. If not, the rally should only last 2-3 weeks and then go back down again. Considering the seasonal tailwinds, I expect a 4-6 week rally towards at least 2870.

SPX 2000

SPX 2007

SPX 2018

Now that I am stuck in a pickle, buying the dip, I will try to wriggle my way out of this mess. There is no way this gap up will be sustainable going into the middle of the US cash session, so I expect sellers to immediately bring down this gap up at 2684,as I am writing, when the US cash market opens. There should be initial support at SPX 2660, and yesterday's lows at 2652. I would wait till after Europe closes, during the US lunch hour to think about buying a dip. If the SPX is below 2660 at that point, it could be a good dip buy looking for an oversold intraday reversal. I hate to do it, but I will need to do some microtrading intraday to try to pick up some points from the bad long entries last week and earlier this week.

There should be a decent intraday bounce coming up after this week is finished, as the stock buybacks will be back with a vengeance starting next week.

Tuesday, October 23, 2018

Panic Opening

Well, that elevated quickly. We finally have the big gap down opening, after countless selling of the gap up opens over the past 2 weeks. It looks panicky out there, and I put in some small buys in the premarket into the carnage. Holding my nose and buying. It is not for the faint of heart, or for the scared, and it looks risky, but we are close to 2700 support, so I like the risk-reward at these levels.

It is notable that in the premarket, the VIX is trading at 24.18, as I write, which is lower than the levels on October 11 and October 12, when the SPX traded higher than current levels. So at least the VIX isn't getting totally out of control.

We have earnings bombs from CAT and MMM, which was foreshadowed by their weak charts. It looks like de-risking ahead of the heart of earnings season, which definitely lowers the bar for upcoming earnings for the big names like MSFT, AMZN, GOOG, INTC later this week.

I am expecting buyers to step in here at the US cash open and should see some reflexive buying off the big gap down open after the weak close yesterday.

It is notable that in the premarket, the VIX is trading at 24.18, as I write, which is lower than the levels on October 11 and October 12, when the SPX traded higher than current levels. So at least the VIX isn't getting totally out of control.

We have earnings bombs from CAT and MMM, which was foreshadowed by their weak charts. It looks like de-risking ahead of the heart of earnings season, which definitely lowers the bar for upcoming earnings for the big names like MSFT, AMZN, GOOG, INTC later this week.

I am expecting buyers to step in here at the US cash open and should see some reflexive buying off the big gap down open after the weak close yesterday.

Monday, October 22, 2018

China Bottoming and Day 13 of Selloff

China came out with some fiscal stimulus in the form of tax cuts to support the economy, and from reports, I am hearing that they are trying to push loans out as fast as possible to reverse the slowdown. I don't think it works in the long run, but it does help sentiment in the short run. Also, Shanghai Composite has gone up 8% over the past 2 trading sessions, so it does look like it has found a short term bottom. I don't think it will go up much from here, as its already rallied a lot, but if it can just stabilize, that will take away one brick from the wall of worry for this market.

Also, Italian 10 year bond (BTP) yields have stabilized after surging higher last week on Italian budget worries. With the ECB unlikely to raise rates for another year, and the huge amount of carry in the Italian BTPs, once the budget concerns die down, there is a lot of room for BTPs to rally. It is not going to be easy to kick Italy out of the EU, and even if they did leave, the Italian central bank would set their yields close to the ECB rate, just because of the state of their economy.

Friday was a tricky session, the fakeout rally in the morning sucked in eager bulls and then chewed them and spit them out into the afternoon and close. It was a classic Friday risk off session, as the sentiment gets worse. From a purely time perspective, this selloff has run its course, and most selloffs in bull markets end by day 13, and I am still considering this a bull market based on the rising 200 day moving average. With the gap up this morning, it probably will get tested by sellers after the US cash market opens, but I expect buyers to show up around the SPX 2760-2770 area, like it has on Thursday and Friday.

This is the heaviest earnings announcement week, so once this week is behind us, there will be a deluge of potential stock buybacks coming. Odds favor the bulls here, so I got long on Friday, and will look to add on any intraday weakness today, to hold for several days.

Also, Italian 10 year bond (BTP) yields have stabilized after surging higher last week on Italian budget worries. With the ECB unlikely to raise rates for another year, and the huge amount of carry in the Italian BTPs, once the budget concerns die down, there is a lot of room for BTPs to rally. It is not going to be easy to kick Italy out of the EU, and even if they did leave, the Italian central bank would set their yields close to the ECB rate, just because of the state of their economy.

Friday was a tricky session, the fakeout rally in the morning sucked in eager bulls and then chewed them and spit them out into the afternoon and close. It was a classic Friday risk off session, as the sentiment gets worse. From a purely time perspective, this selloff has run its course, and most selloffs in bull markets end by day 13, and I am still considering this a bull market based on the rising 200 day moving average. With the gap up this morning, it probably will get tested by sellers after the US cash market opens, but I expect buyers to show up around the SPX 2760-2770 area, like it has on Thursday and Friday.

This is the heaviest earnings announcement week, so once this week is behind us, there will be a deluge of potential stock buybacks coming. Odds favor the bulls here, so I got long on Friday, and will look to add on any intraday weakness today, to hold for several days.

Friday, October 19, 2018

BTFD Fridays

With the market acting skittish, but unable to make substantial down moves, I will be looking to buy weakness off this gap up towards SPX 2770. There seems to be a lot of support in the 2760-2770 area, and the selling has dried up whenever it reaches that price level. If the market manages to pullback towards the closing price zone of 2765-2770, I will be an eager buyer today.

Usually you don't get gap and go moves higher on Friday, especially on options expiration day, so I expect some kind of pullback at the open. I doubt we get continuation selling, just based on closing price action yesterday and the ease with which the SPX is adding on points in the premarket. A continuation of the selling from yesterday is usually signified by a close near the lows of the day, or at least a gap down from the middle of the afternoon trading range (2758-2786).

Traders seem well hedged as the options volume has been elevated for the last several days. That should allow for more aggressive buying from fund managers for the next few weeks. That also coincides with the return of stock buybacks. Leaning bullish for the intermediate term.

Usually you don't get gap and go moves higher on Friday, especially on options expiration day, so I expect some kind of pullback at the open. I doubt we get continuation selling, just based on closing price action yesterday and the ease with which the SPX is adding on points in the premarket. A continuation of the selling from yesterday is usually signified by a close near the lows of the day, or at least a gap down from the middle of the afternoon trading range (2758-2786).

Traders seem well hedged as the options volume has been elevated for the last several days. That should allow for more aggressive buying from fund managers for the next few weeks. That also coincides with the return of stock buybacks. Leaning bullish for the intermediate term.

Thursday, October 18, 2018

Too Late To Short

Sometimes patience is a good thing, but this time waiting to short was a mistake, and we are down over 50 SPX points from the close and increasing. Its been a week of missed opportunities, but if the selling gets extreme enough to take the SPX down to 2750, I will be interested in buying that dip. We'll see how the afternoon trade goes, but since I missed the short, I will look to get long on further selling. Unless this sell cycle turns into a month long affair, this second sell wave should be finished by Friday, as that will be trading day 12 of the selloff. That is a common length (12-13 trading days) for a selloff in the past. After this week, the market will likely grind higher as the stock buybacks slowly come back.

I am not ready to get super bearish on this market yet, the seasonal effects will be a marginal positive for the stock market, so I will wait for later this year/early next year to put on long term shorts for a big down move.

I am not ready to get super bearish on this market yet, the seasonal effects will be a marginal positive for the stock market, so I will wait for later this year/early next year to put on long term shorts for a big down move.

Wednesday, October 17, 2018

Timing Off By a Day

There is still that fear of missing out on the next uptrend, even during a topping process. It will provide the bounces that are profitable to short for the next few months. There is an upside and a downside to the tendency to panic quickly, both on the way down and on the way up. The upside is that it provides more short term trading opportunities. The downside is that the jumpy, quantum leaps up and down make it riskier to fade the short term trend with leveraged positions. Essentially, due to the low bucket shop margin requirements, futures trading is hyper leveraged trading disguised as a hedging tool.

What happened on Tuesday was what I was expecting for Monday, so when Monday was actually a down day, I rewrote the trading plan and it cost me. Just because my timing was off. There were a lot of points to be made on Tuesday that I missed because I doubted my previous forecast because of one small down day. I did not expect the market to delay the oversold rally by a day, skipping Monday and instead deciding that Tuesday was a better day to buy.

Sometimes these things happen, when I forecast the market to go a certain direction, and when it doesn't happen in the expected time frame, I change the forecast. Often times, the forecast is correct, just the timing is off by a few days, as the market takes its time when making a move. That doesn't match my general observation that the markets in recent years move faster towards their price targets and don't give traders much time to jump on board the trend.

There is a lesson to be learned from this. It is to to put on a position a little early, even just 1/3 to 1/2 size, just in case my forecast for the timing of a move is off by a day or two.

Now that SPX is above 2800, we are right in the post panic sell area. If the SPX stays under 2840 this week, that rules out a V bottom, and we should look to short on Friday for a move back down to 2740-2750 for next week. Just to stay out out potential trouble in a V bottom scenario, I will not be shorting today or tomorrow. I don't want to go long unless there is another flush out of yesterday's buyers. So nothing much to do in SPX for the next 2 days.

What happened on Tuesday was what I was expecting for Monday, so when Monday was actually a down day, I rewrote the trading plan and it cost me. Just because my timing was off. There were a lot of points to be made on Tuesday that I missed because I doubted my previous forecast because of one small down day. I did not expect the market to delay the oversold rally by a day, skipping Monday and instead deciding that Tuesday was a better day to buy.

Sometimes these things happen, when I forecast the market to go a certain direction, and when it doesn't happen in the expected time frame, I change the forecast. Often times, the forecast is correct, just the timing is off by a few days, as the market takes its time when making a move. That doesn't match my general observation that the markets in recent years move faster towards their price targets and don't give traders much time to jump on board the trend.

There is a lesson to be learned from this. It is to to put on a position a little early, even just 1/3 to 1/2 size, just in case my forecast for the timing of a move is off by a day or two.

Now that SPX is above 2800, we are right in the post panic sell area. If the SPX stays under 2840 this week, that rules out a V bottom, and we should look to short on Friday for a move back down to 2740-2750 for next week. Just to stay out out potential trouble in a V bottom scenario, I will not be shorting today or tomorrow. I don't want to go long unless there is another flush out of yesterday's buyers. So nothing much to do in SPX for the next 2 days.

Tuesday, October 16, 2018

Weak Bounce

Heading into this week, I was looking for a bounce to take up to at least SPX 2800, as the market seemed to have flushed out the weak hands in the short term. But the lack of follow through buying and the weakness overnight was an omen. Clearly, investors don't have FOMO here and are not ready to take any risks chasing strength here.

Monday should have been an up day, with short term traders looking to buy the dip to start the week, after the panic last week finally subsided, with a V bottom on Friday. But the intraday bounces were sold and the put/call ratios went back to normal levels, not a great sign.

You can forget about the V bottoms that you saw with regularity from 2009 to 2014. We are in the messy bottom phase of the stock market cycle, similar to 2015, and earlier this year. This market can't hang on to strength without stock buybacks to fuel the buying power. There are many that are skeptical about the seasonal effects of the buyback blackout period on stock market performance, but the data is right there if you look for it. When retail is still a net seller of equities and fund managers don't have the inflows, they don't have the buying power to support the market. Pensions are becoming a smaller part of the buying pool and have a much smaller effect on the market these days. The main buyer of stocks are the companies themselves. This makes any earnings downturn deadly for stocks, because these companies won't be able to borrow money at decent rates to buy back their stock, and will have less cashflow to direct towards supporting their share price.

A note on the bond market. There was a below consensus CPI number on Thursday and weak retail sales number on Monday, and the SPX has gone down 180 points from the highs. And the 10 year yield is still lingering near the highs, at 3.17%. The lack of a flight to safety bid for Treasuries is the most important thing that no one is mentioning over the past week. Remember, this whole pullback started because the 10 year started breaking out to new highs, and that monkey is still on the stock market's back. Once the buybacks comeback starting in late October and the stock market bounces, look out for a potential ugly selloff in Treasuries.

The game plan for trading the SPX is either to put on a small short on a bounce towards 2780-2790 either today or Wednesday, or wait for the next sell wave to complete and buy around 2680-2700 later this week. Not expecting much to happen today, probably just chop around the range traded on Monday.

Monday should have been an up day, with short term traders looking to buy the dip to start the week, after the panic last week finally subsided, with a V bottom on Friday. But the intraday bounces were sold and the put/call ratios went back to normal levels, not a great sign.

You can forget about the V bottoms that you saw with regularity from 2009 to 2014. We are in the messy bottom phase of the stock market cycle, similar to 2015, and earlier this year. This market can't hang on to strength without stock buybacks to fuel the buying power. There are many that are skeptical about the seasonal effects of the buyback blackout period on stock market performance, but the data is right there if you look for it. When retail is still a net seller of equities and fund managers don't have the inflows, they don't have the buying power to support the market. Pensions are becoming a smaller part of the buying pool and have a much smaller effect on the market these days. The main buyer of stocks are the companies themselves. This makes any earnings downturn deadly for stocks, because these companies won't be able to borrow money at decent rates to buy back their stock, and will have less cashflow to direct towards supporting their share price.

A note on the bond market. There was a below consensus CPI number on Thursday and weak retail sales number on Monday, and the SPX has gone down 180 points from the highs. And the 10 year yield is still lingering near the highs, at 3.17%. The lack of a flight to safety bid for Treasuries is the most important thing that no one is mentioning over the past week. Remember, this whole pullback started because the 10 year started breaking out to new highs, and that monkey is still on the stock market's back. Once the buybacks comeback starting in late October and the stock market bounces, look out for a potential ugly selloff in Treasuries.

The game plan for trading the SPX is either to put on a small short on a bounce towards 2780-2790 either today or Wednesday, or wait for the next sell wave to complete and buy around 2680-2700 later this week. Not expecting much to happen today, probably just chop around the range traded on Monday.

Monday, October 15, 2018

Panicking More Quickly

The US stock market behavior has changed since 2008. The jumpiness of the VIX has increased dramatically. A look at the numbers since 2007 show that during the first big correction in 2007, on August 16, the VVIX closed at 142.99. In the height of the financial panic in 2008, the highest VVIX close was 134.87 on October 27. In 2009, it never closed above 105. In 2010, a couple of weeks after the flash crash on May 20, it closed at 145.12. In 2011, during the middle of the European sovereign bond crisis, it closed at 134.63 on August 8. In 2015, the VVIX hit a record close of 168.75 on August 24. In 2018, the record was broken on February 5 when VVIX closed at 177.34, after hitting an intraday high of 203.73.

It is quite telling, that even during the biggest bear market of our lifetime from 2007 to 2009, the highest VVIX close was 142.99, while milder corrections in 2015 and 2018 resulted in much higher VVIX readings.

It struck again when the VVIX jumped up to 147 intraday last Thursday as the SPX hit 2712, down just 7% off all time high.

These high VVIX readings this year is an indication of how offsides the investment community was in regards to SPX downside risk. The fund managers have been lulled to sleep over the low VIX readings since May. It takes time for them to adjust to the new volatility regime, more than the 7 days since the beginning of the selloff from 2925 on Thursday, October 4. It has been 7 trading days since. Usually for big drops like this, it usually takes at least 12-13 trading days for fund managers to hedge themselves and lower risk to adjust for the higher volatility, and for weak hands to get stopped out. So this should be another week where bounces will be brief and sold quickly.

As I writing in premarket, the SPX is already over 20 points off the close on Friday, on no news, and negating the intraday reversal pattern. It was a fakeout reversal on Friday, a combination of short covering at the close and eager bulls piling in hoping to catch the bottom. I am still looking for 2680-2700 area as a buyable zone, but with the recent jumpiness in this market, and the herdlike behavior of the systems traders, I won't rule out a monster flush out towards 2600. This is no longer the kiddie zone of the pool. We are in the deep end, sharks are lurking waiting to feed on the weak handed fish. Right now, the longs are the fish. Next week, it probably will be the shorts.

With the big gap down on a Monday, I do expect intraday day buying off these levels from short term traders which likely pushes the market towards the Friday close of SPX 2767. If SPX is below 2767 by 3:00 PM ET, then we'll probably see a weaker close as traders will want to lower long exposure ahead of overnight risk, and the sell bots will swarm this market back down towards the 2740s.

SPX will have trouble going above the Thursday highs of 2794 this week. It is still safer to sell the bounces than try to buy the dips here. The selloff has not fully matured yet, give it another 5 trading days and we'll reevaluate where we've hit bottom then.

It is quite telling, that even during the biggest bear market of our lifetime from 2007 to 2009, the highest VVIX close was 142.99, while milder corrections in 2015 and 2018 resulted in much higher VVIX readings.

It struck again when the VVIX jumped up to 147 intraday last Thursday as the SPX hit 2712, down just 7% off all time high.

These high VVIX readings this year is an indication of how offsides the investment community was in regards to SPX downside risk. The fund managers have been lulled to sleep over the low VIX readings since May. It takes time for them to adjust to the new volatility regime, more than the 7 days since the beginning of the selloff from 2925 on Thursday, October 4. It has been 7 trading days since. Usually for big drops like this, it usually takes at least 12-13 trading days for fund managers to hedge themselves and lower risk to adjust for the higher volatility, and for weak hands to get stopped out. So this should be another week where bounces will be brief and sold quickly.

As I writing in premarket, the SPX is already over 20 points off the close on Friday, on no news, and negating the intraday reversal pattern. It was a fakeout reversal on Friday, a combination of short covering at the close and eager bulls piling in hoping to catch the bottom. I am still looking for 2680-2700 area as a buyable zone, but with the recent jumpiness in this market, and the herdlike behavior of the systems traders, I won't rule out a monster flush out towards 2600. This is no longer the kiddie zone of the pool. We are in the deep end, sharks are lurking waiting to feed on the weak handed fish. Right now, the longs are the fish. Next week, it probably will be the shorts.

With the big gap down on a Monday, I do expect intraday day buying off these levels from short term traders which likely pushes the market towards the Friday close of SPX 2767. If SPX is below 2767 by 3:00 PM ET, then we'll probably see a weaker close as traders will want to lower long exposure ahead of overnight risk, and the sell bots will swarm this market back down towards the 2740s.

SPX will have trouble going above the Thursday highs of 2794 this week. It is still safer to sell the bounces than try to buy the dips here. The selloff has not fully matured yet, give it another 5 trading days and we'll reevaluate where we've hit bottom then.

Friday, October 12, 2018

First Wave of Selling Done

They don't make this game easy. I was waiting for a puke out in the final hour of SPX trading to buy, instead there was a fakeout rip higher to 2760 and then a fade of that rip back down to 2730. And then a bounce off the 2730 area right back to 2750 in just 15 minutes into the futures close at 4:15 pm ET. And its been off to the races since then. So this is not a repeat of February. This is the junior version of that selloff. More traders were more cautious this time around then back in January/February, so the selloff should be less severe. Plus the seasonals favor the bulls starting next week.

The most important time of the day isn't the final 15 minutes of cash trading, its the 15 minutes from cash close to futures close, from 4:00 pm to 4:15 pm ET. That aggressive buying out of nowhere was likely sell bots that had sold the last 15 minutes of the cash close, expecting further weakness into the futures close at 4:15, and instead sold a bounce and got stopped out and exited all at once.

The trade from 4:00 to 4:15 has been a foreshadow of what is to happen in the overnight session. On Wednesday, the weakness in the last 15 minutes of futures trading spilled over into the overnight session. On Thursday, the strength in the last minutes has continued overnight. The bounce off the lows emboldens the BTFDer who now believes that we've hit bottom, and they are piling into the futures overnight.

It appears like the first wave of selling is finished and we can look foward to a bounce in the coming days. Looking at a 50% retrace of the down move from 2940 to 2710, is 2825. So roughly 2825 is the target for any bounce early next week. After that bounce, expecting the second wave of selling and a more lasting bottom to be hit, somewhere around 2680-2700. With the velocity of moves in the bot era, 2825 to 2700 could happen over just 2 trading days.

Friday's US cash session should provide one good selloff to buy, not sure whether that will be in the morning or in the afternoon. I would be surprised to see a gap and go trade, as traders usually don't want to get aggressively long over the weekend after such a bad week.

Thursday, October 11, 2018

Algos Looking for Blood

2018 has been an all or nothing year. Either up continuously or down continuously. Unlike past corrections in prior years, the market has tended to do nothing for months, trade with low volatility, and then suddenly, one day, the volatility explodes. There were no 1% moves for over 3 months and then suddenly you have an over 3% whopper and now another 1% lower in premarket just to kick the BTFDer while he's down.

The CTAs and the hedge funds are all in the same trades, enter gradually into their positions, but puke them out all at once. It happened in February, and it is happening again. Both times due to higher interest rates.

The HFT algos are like sharks sensing blood in the water. They are predatory and very profitable. Especially on big down days. The institutions who are panicking and dumping stock are being ruthlessly front run and are either forced to puke out at rock bottom prices or can't get out. It is a roach motel market now.

I am out of the short, and will wait for lower prices before putting on longs. Clearly the velocity of the selling into yesterday's close made 2800 look like it was nothing. Now it is on to 2700, and then 2675, the closing level of 2017. Beware of trying to buy the dip on Thursday. The market has changed character and traders like to liquidate and panic on Thursday afternoons and Friday mornings, getting ahead of the "afraid of being long over the weekend" crowd. It doesn't wait for Friday afternoon anymore to panic sell weakness.

It is going to be wild trading over the next few days. With bonds not providing a good diversifying hedge for equities, it puts more pressure on portfolio managers, many of them running 60/40 stock/bond allocations, who don't know how to deal with big down days as bonds aren't providing a safety valve for their stock holds. Risk parity pressures are going to be a weight on this market so don't expect a run right back towards 2900 like nothing happened. The damage is real this time. While we will likely get a year end rally, there is no need to rush into any longs at this point. Let the algos do their job.

If SPX opens at current overnight levels, around 2750, you should get a reflexive buy program in the first hour, taking it up to yesterday's close at 2785, and consolidate that move for a couple of hours and then selloff again in the afternoon, as longs get scared of holding overnight and also over the weekend and beating the Friday panic selling crowd. A weak close today and a gap down on Friday will likely set a temporary bottom on Friday.

Wednesday, October 10, 2018

The Fed: Always Late to the Party

In the past few weeks, you have had a wave of Fed speakers give hawkish speeches, chiefly the boss, Jerome Powell. You would figure that with all this hawkish talk, the Fed would actually consider raising more than 25 bps every 3 months, but central banks have been mostly talk, little action.

It has been an excruciating rate hiking cycle, starting in 2014 with a Please Hammer, Don't Hurt 'em MC Hammer style slow QE taper, when the US economy was at its post 2008 peak. The taper should have never happened. It just delayed the start of rate hikes by over a year, and when the US economy finally started slowing down in late 2015, the Fed reluctantly raised once and froze in the face of a slowdown, with Fed funds stuck at 0.25-0.50%.

The delay of Fed tightening just allowed more corporate debt to build up and the stock market to reach levels of overvaluation rivaling 2000. The short term thinking at the Fed, overstaying easy monetary policy and slow to tighten when the economy improves, has resulted in longer, more tepid booms, but also bigger busts. When stock prices get this overvalued, they eventually lead to a bear market, and that will be the trigger for a recession. Ever since 2000, the US economy has basically been the stock market. The stock market is the tail wagging the US economy dog. There is no real wage growth, so a strong economy won't boost consumption. It will just make the rich richer, and lead to higher inflation. That is why there always seem to be a bit of skepticism in regards to the US equity bull market, because it just doesn't match the low growth economy.

That being said, the current US GDP growth rate is not long term sustainable. It took a strong US bull market, big tax cuts, with a huge increase in government spending to get to 4% GDP growth. That isn't happening again next year. Economy is cyclical, and high PMIs and consumer confidence numbers mean that people and companies are spending now, which makes them likely to spend less in the future.

Back to the Fed. They are finally catching up to what the economy has been for the last 18 months. All this hawkish rhetoric should have been said in the beginning of 2017, not now. The Fed is already behind the curve. The Fed funds rate should have been at 3.00% for the last 12 months. Now they probably can't make it to 3.00% before the SPX has a big correction, which would immediately freeze the rate hikes. And once they freeze the rate hikes, since the Fed funds is now near neutral, they won't be able to hike anymore.

That is why you have been seeing the yield curve bear steepening, because the bond market is sniffing out future equity market weakness. While that can be right in the very short term, beyond the next couple of weeks, I see a flattening. I don't think the stock market can fall too much because the majority of stock buybacks, nearly 25%, happen in the last 2 months of the year. That gives the bears about 2 weeks to make their move, and then it will be the bulls taking control with buybacks fueling it. That should cause the curve to flatten back out in November and December. Right now is probably the ideal time to put on a 5-30s flattener, at 32 bps, with expectation that it will go back to the level seen in August, around 21 bps.

Monday, October 8, 2018

Corporate Welfare Delaying the Bear

The Fed reducing their balance and raising rates should have kicked off the bear market this year, were it not for some serious fiscal stimulus, most of it geared to help corporate profits. Low tax cash repatriation was the first wave of money that corporations were given. This was promptly used to buy back stock. The next wave, which will last for a while, is the lower corporate taxes, which gives corporations more capital for guess what? Stock buybacks, and the occasional PR savvy one time $1000 bonuses to all workers. There is a big difference between a $1000 bonus and a permanent wage increase, which most companies are loathe to do, and really don't have to. When you have an oligopoly, like most US multinationals do at the moment, there is no wage pressure. It is take it or leave it for the worker. They usually don't have anywhere else to go. And although they say the labor market is tight, its only because the wages haven't gone up and the labor force isn't growing. Workers have very little pricing power, unions are weak or nonexistent, and there aren't many competitors that workers can switch to.

An oligopoly not only gives you pricing power on goods, it also gives you pricing power on labor. With the relentless trend towards mergers and acquisitions, and reduced competition, companies are enjoying the benefits of increased pricing power, which obviously leads to increases profit margins.

Rent seeking is the ideal corporate business model, because there is no need to spend money on R&D, you can just raise prices and reap the benefits. And competitors don't show up because these corporations now spend more money on lobbyists and campaign financing, to ensure the moats around their oligopolies, to increase the barriers to entry via specific, pinpoint government regulation, demanded by the corporate lobbyists. The US Government has now become ensnared in an arm of the corporate "vampire squid", which provide the financing to politicians, who need the money to get elected, and thus compensate the corporations with favorable rules and regulations.

This trend towards corporate welfare will not be easy to break. It has been happening since the 1980s, under both Republicans and Democrats. Populism will only help the corporations even more, in a roundabout manner. Because populism requests handouts, and handouts mean bigger budget deficits, which eventually leads to a weaker dollar, due to the eventual requirement of low interest rates Fed intervention and QE to suck up all that debt issuance. And a weaker dollar hurts the consumer, and helps the corporations.

The current financial situation is not a stable equilibrium. Only through the sheer force of the fiscal stimulus (both tax cuts and big budget increases) has the market been able to overcome Fed tightening. This gives the market a false sense of confidence, and attitude of invincibility. The money noose is getting tighter and tighter, and the fiscal stimulus is now reflected in corporate profit estimates.

Looking at the consumer confidence numbers, they usually peak with the economic cycle, and it is looking like late 1999/early 2000, both from an economic data and financial markets perspective. The SPX and bond yields should top out later this year, probably around December, after the flood of stock buybacks get to work.

We have a little weakness the past few days based on the rapid rise in rates, but that usually doesn't last. The stock market can only fall hard on its own weight, not from external factors. Give it a couple more months and it will be bull hunting season.

There is no need to short in the hole and sell after a pullback. There will be plenty of rallies to sell into later this year. For very aggressive traders, a deeper pullback towards 2800-2820 would be a buy opportunity to sell later into a November rally.

An oligopoly not only gives you pricing power on goods, it also gives you pricing power on labor. With the relentless trend towards mergers and acquisitions, and reduced competition, companies are enjoying the benefits of increased pricing power, which obviously leads to increases profit margins.

Rent seeking is the ideal corporate business model, because there is no need to spend money on R&D, you can just raise prices and reap the benefits. And competitors don't show up because these corporations now spend more money on lobbyists and campaign financing, to ensure the moats around their oligopolies, to increase the barriers to entry via specific, pinpoint government regulation, demanded by the corporate lobbyists. The US Government has now become ensnared in an arm of the corporate "vampire squid", which provide the financing to politicians, who need the money to get elected, and thus compensate the corporations with favorable rules and regulations.

This trend towards corporate welfare will not be easy to break. It has been happening since the 1980s, under both Republicans and Democrats. Populism will only help the corporations even more, in a roundabout manner. Because populism requests handouts, and handouts mean bigger budget deficits, which eventually leads to a weaker dollar, due to the eventual requirement of low interest rates Fed intervention and QE to suck up all that debt issuance. And a weaker dollar hurts the consumer, and helps the corporations.

The current financial situation is not a stable equilibrium. Only through the sheer force of the fiscal stimulus (both tax cuts and big budget increases) has the market been able to overcome Fed tightening. This gives the market a false sense of confidence, and attitude of invincibility. The money noose is getting tighter and tighter, and the fiscal stimulus is now reflected in corporate profit estimates.

Looking at the consumer confidence numbers, they usually peak with the economic cycle, and it is looking like late 1999/early 2000, both from an economic data and financial markets perspective. The SPX and bond yields should top out later this year, probably around December, after the flood of stock buybacks get to work.

We have a little weakness the past few days based on the rapid rise in rates, but that usually doesn't last. The stock market can only fall hard on its own weight, not from external factors. Give it a couple more months and it will be bull hunting season.

There is no need to short in the hole and sell after a pullback. There will be plenty of rallies to sell into later this year. For very aggressive traders, a deeper pullback towards 2800-2820 would be a buy opportunity to sell later into a November rally.

Friday, October 5, 2018

A Different Bond Bear Market

This is not your 2013 bond bear market. Or the 2006 bear market. You have to go back to late 1999/early 2000 bear market to get anywhere close to this kind of protracted selloff in bonds. Ironically, the turtle like pace at which the Fed has chosen for this rate hike cycle has only lengthened the bearish phase. And according to Eurodollar futures, the Fed is priced to hike at least 3 more times before they finish.

I have been skeptical about the Fed raising rates as much as the STIRs market has priced in, but they have gone beyond market expectations, and Powell is clearly not into dovish moves like Bernanke and Yellen. The US economy is holding on with steady growth, although the leading indicators point to a softer economy in 2019. In 2000, the 10 year yield topped out in January, 4 months before the last rate hike in May. In 2006, the 10 year yield made an initial top right around the last rate hike in June 2006, and then retested that top a year later in June 2007. The only reason that bond bear market was stretched out into June 2007 was because the stock market kept grinding higher with commodities prices and made bond investors nervous about potentially more hikes down the line. The economy had already peaked out several months before June 2007.

So what will end this bond bear market?

1. SPX has to go down. The first and most important component is the stock market. There are two economies now in the US. The top 10% economy, and then the 90% economy. The top 10% own a lot of US stocks and other assets, so their economy is sensitive to the stock market. The other 90% is stuck in a deep malaise that is stagnant and mostly insensitive to the stock market. In fact, they would be better off with a weaker stock market and lower housing prices and lower inflation, because their wages aren't keeping up with increasing prices for services.

2. Be within 2 meetings of the end of a Fed hiking cycle. Since the Fed seems to be on a quarterly hiking schedule, the market has to sense that the next rate hike is the last one. That will bring in the sidelined money that feared the uncertainty of future rate hikes. Right now, it seems like Powell wants to raise at least once more, in December, for sure, and probably 2 more times next year as long as the stock market doesn't meltdown. So this is somewhat related to what the SPX does next year.

3. Chinese economy getting worse. Europe and Japan have been zombiefied so they are living corpses that occasionally show a pulse but rarely move the needle. A Chinese debt or currency crisis would be a game changer for the world economy. Even without a crisis, if China enters into the 1990s Japan phase of their economic cycle, low growth will be a drag on the global economy and increase demand for bonds.

We still don't have the SPX showing clear weakness, although initial signs of topping can be seen in market internals, as new 52 week lows expand at both the Nasdaq and NYSE. Powell still seems hell bent on hiking till something breaks. The highest probably situation is China getting worse, which then spills over to SPX weakness, leading to Powell stopping rate hikes. That could be a 2019 story. The rest of this year should be relatively calm as China is pumping in a ton of liquidity, cramming money down state owned enterprises' throats, which should at least keep Humpty Dumpty together for a few more months.

As for the current market, we are in the middle of a pullback that should be more vicious than the one we saw in early September. The complacency is higher now and the market internals are worse. SPX 2870 support has held on the first test today, but it doesn't look like it will stop there. Thinking SPX 2800-2810 is definitely possible within the next 2 weeks.

I have been skeptical about the Fed raising rates as much as the STIRs market has priced in, but they have gone beyond market expectations, and Powell is clearly not into dovish moves like Bernanke and Yellen. The US economy is holding on with steady growth, although the leading indicators point to a softer economy in 2019. In 2000, the 10 year yield topped out in January, 4 months before the last rate hike in May. In 2006, the 10 year yield made an initial top right around the last rate hike in June 2006, and then retested that top a year later in June 2007. The only reason that bond bear market was stretched out into June 2007 was because the stock market kept grinding higher with commodities prices and made bond investors nervous about potentially more hikes down the line. The economy had already peaked out several months before June 2007.

So what will end this bond bear market?

1. SPX has to go down. The first and most important component is the stock market. There are two economies now in the US. The top 10% economy, and then the 90% economy. The top 10% own a lot of US stocks and other assets, so their economy is sensitive to the stock market. The other 90% is stuck in a deep malaise that is stagnant and mostly insensitive to the stock market. In fact, they would be better off with a weaker stock market and lower housing prices and lower inflation, because their wages aren't keeping up with increasing prices for services.

2. Be within 2 meetings of the end of a Fed hiking cycle. Since the Fed seems to be on a quarterly hiking schedule, the market has to sense that the next rate hike is the last one. That will bring in the sidelined money that feared the uncertainty of future rate hikes. Right now, it seems like Powell wants to raise at least once more, in December, for sure, and probably 2 more times next year as long as the stock market doesn't meltdown. So this is somewhat related to what the SPX does next year.

3. Chinese economy getting worse. Europe and Japan have been zombiefied so they are living corpses that occasionally show a pulse but rarely move the needle. A Chinese debt or currency crisis would be a game changer for the world economy. Even without a crisis, if China enters into the 1990s Japan phase of their economic cycle, low growth will be a drag on the global economy and increase demand for bonds.

We still don't have the SPX showing clear weakness, although initial signs of topping can be seen in market internals, as new 52 week lows expand at both the Nasdaq and NYSE. Powell still seems hell bent on hiking till something breaks. The highest probably situation is China getting worse, which then spills over to SPX weakness, leading to Powell stopping rate hikes. That could be a 2019 story. The rest of this year should be relatively calm as China is pumping in a ton of liquidity, cramming money down state owned enterprises' throats, which should at least keep Humpty Dumpty together for a few more months.

As for the current market, we are in the middle of a pullback that should be more vicious than the one we saw in early September. The complacency is higher now and the market internals are worse. SPX 2870 support has held on the first test today, but it doesn't look like it will stop there. Thinking SPX 2800-2810 is definitely possible within the next 2 weeks.

Thursday, October 4, 2018

Financials are the Canaries

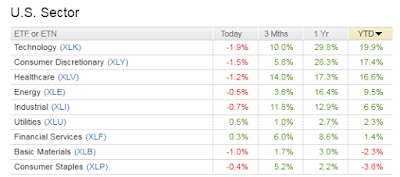

Sector analysis is usually not very helpful in determining market direction, because the market often doesn't follow the economy. According to Ned Davis Research, since 1970, the best performing sectors in the 3 months leading up to a bull market top are health care, consumer discretionary, and consumer staples. The worst performing sectors in the 3 months ahead of a top are financials, utilities, and energy.

Here are the last 3 month and YTD performances for the biggest US sectors:

While the last 3 months are a mixed bag as far as signaling a bull market top, the YTD performance clearly shows that financials and utilities have underperformed the S&P 500, and health care and consumer discretionary have outperformed the S&P 500. What is especially notable is the weakness in the financials, because rising rates are supposed to be great for banks, increasing their net interest margin, but banks have been lagging all year, and have only started going up recently after the 10 year yield has rocketed higher for the past month. It is still barely up for the year, despite having massive stock buybacks and a 10 year yield that's gone up from 2.40% to 3.20%.

There are also the cluster of Hindenburg Omens that I mentioned last month which continues, as new lows continue to expand despite the market being close to all time highs. Add to that the pressure of higher yields and being in a blackout period for stock buybacks and you have a market that is vulnerable to a selloff. We are seeing that today and although I don't expect anything big on the downside, with decent support around the January highs and September lows of 2870, the probability of a quick plunge like you saw in February is getting higher. However, you still have positive end of year forces that will likely push stocks higher in November and December if we do get a pullback this month. We are nearing the end game for this 10 year bull market as a growing number of warning signs are flashing.

Here are the last 3 month and YTD performances for the biggest US sectors:

While the last 3 months are a mixed bag as far as signaling a bull market top, the YTD performance clearly shows that financials and utilities have underperformed the S&P 500, and health care and consumer discretionary have outperformed the S&P 500. What is especially notable is the weakness in the financials, because rising rates are supposed to be great for banks, increasing their net interest margin, but banks have been lagging all year, and have only started going up recently after the 10 year yield has rocketed higher for the past month. It is still barely up for the year, despite having massive stock buybacks and a 10 year yield that's gone up from 2.40% to 3.20%.

There are also the cluster of Hindenburg Omens that I mentioned last month which continues, as new lows continue to expand despite the market being close to all time highs. Add to that the pressure of higher yields and being in a blackout period for stock buybacks and you have a market that is vulnerable to a selloff. We are seeing that today and although I don't expect anything big on the downside, with decent support around the January highs and September lows of 2870, the probability of a quick plunge like you saw in February is getting higher. However, you still have positive end of year forces that will likely push stocks higher in November and December if we do get a pullback this month. We are nearing the end game for this 10 year bull market as a growing number of warning signs are flashing.

Subscribe to:

Comments (Atom)