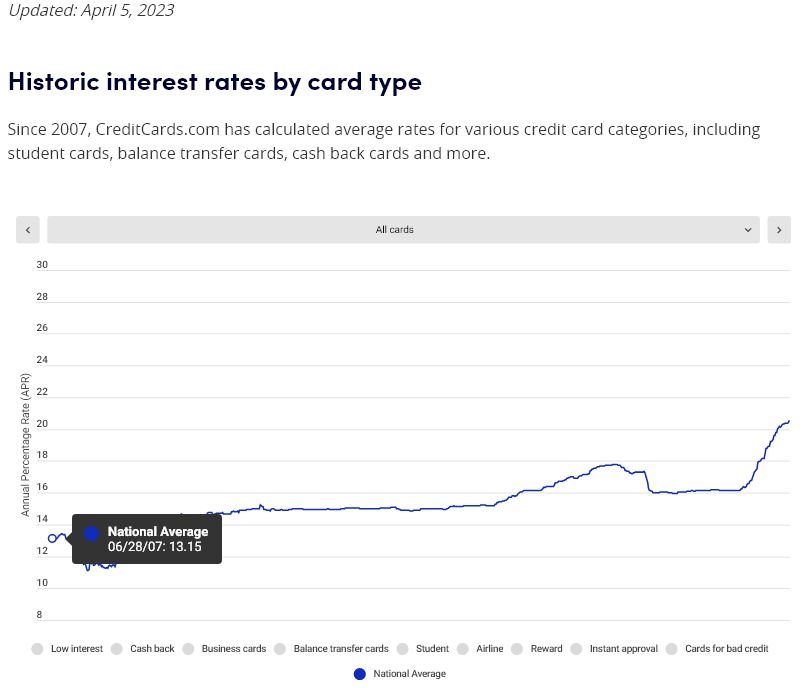

I find it interesting that credit card debt has gone from 13.15% in June 2007, when Fed funds rate was at 5.25%, and is now at 20.35% in April 2023, with Fed funds rate at 4.83%. Over the course of 16 years, credit card issuers have fattened up their profit margins.

The stock market isn't really a reflection of the economy, its a reflection of corporations' ability to generate cash flow. The biggest corporate expense is from labor. The median wage to GDP/capita ratio has been trending down for the last 40 years. A boon for corporate profit margins. Globalization leads to wage arbitrage, and corporations gain a big advantage over labor with fewer corporate competitors for that labor.

As much as people like to hype up deglobalization, its bunk. The long term trend of higher Chinese exports continues.

Unless you get a lot more anti trust enforcement, a lot more corporate competition in the US, and a lot less favorable tax regime for corporations and the wealthy, the long term demand for stocks will be there, either from institutions or from companies themselves. Of course, this favorable situation for corporate America is reflected in fat profit margins, which were at a historic high just a year ago, and historically high valuations. This is why its very unlikely you will ever get to anything resembling cheap valuations in the SPX. My base case scenario which is an old fashioned credit tightening led recession, SPX probably bottoms around last year's lows of 3500-3600. I just don't see the SPX going down towards 3000-3200 like some of the bears out there. There is just too much liquidity and cash sloshing around.

Unlike 2022, its not a slam dunk to short rallies anymore. Even though the economy is definitely weaker this year than last year. Valuations are high, so upside is limited, but cash levels are also high, which means there are a lot of potential buyers waiting to pounce at lower valuations. Corporations are still doing a ton of buybacks, providing a consistent bid for the market. I would still lean short here if I had to choose a position right now for the next 6 month, due to the economic weakness which is being underestimated.

This week went a long way towards correcting the misperception out there that the consumer is strong, that the US economy is not close to a recession. The leading indicators are finally starting to work their way into the coincident indicators like employment. This time, its very unlikely to be a headfake like December 2022, when we had a similar shift in investor perceptions on the economy towards recession. Short rates are even higher now, the jobs market is starting to soften, and banks are much tighter with credit and lending.

The analysts and fund managers that come on TV have turned more cautious on the economy, but they still think that the Fed won't cut rates this year due to high inflation. But the leading indicators for inflation are coming down.

The Fed are like bad traders, they can't sit still. They've made a bad trade by repeating the transitory inflation lie and cutting too late, and followed that up with another bad trade by overreacting to lagging data and overhiking. Now they will make another mistake, which will be to not proactively cut rates, waiting for the lagging indicators to tell them that its ok to cut, which will be way too late. A lot of damage has been done. The longer the Fed delays rate cuts, it just accumulates even more damage.

Investors suddenly seem gloomy again, with those weak ISM numbers and low ADP stoking recession fears. Its tempting to see those weak economic numbers and go short, expecting an imminent downtrend, but I'm cautious about the Fed pivot fueling one last short squeeze and hedge fund chase for performance. And there is also the risk that a lower than expected CPI number next week could fuel another euphoric move higher. So I remain mostly in cash, with some bonds. I would be a buyer of dips in the short end in fixed income and a seller of rips around SPX 4200. Tech and retail favorites are preferred short targets.

2 comments:

Sold BOIL Jun 3 calls @ .90

Long LUNR 10.55

What's the source of VP CPI data? And what does it represent?

Post a Comment