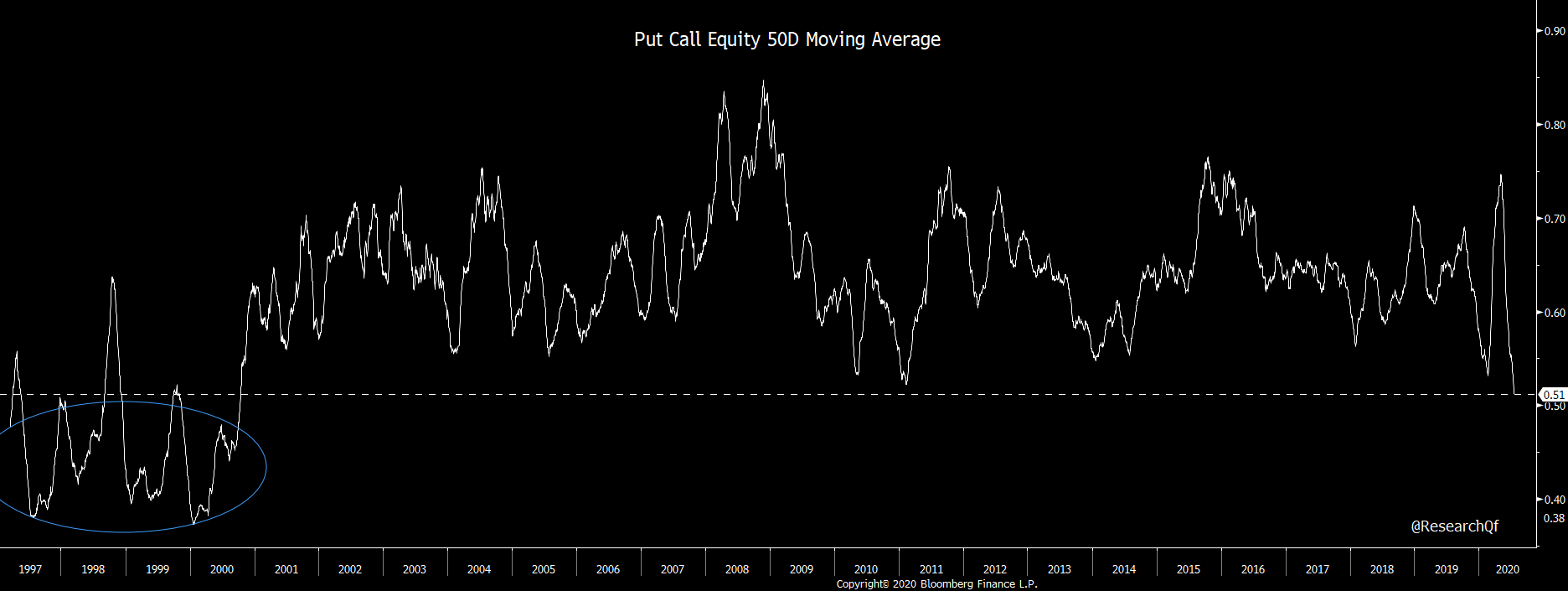

Robinhood traders, the butt of traders' jokes, have recently been viewed as astute, and trading better than hedge funds, as they have piled into big cap tech as well as momos like TSLA, and pump and dumps that have been remarkably resilient (NIO, WKHS, etc).

Let's not confuse brains with a bull market. And let's not

extrapolate the short term with the long term. Investing/trading is a

long term game, even if it seems like everyone is just focused on the

move over the next hour/day/week.

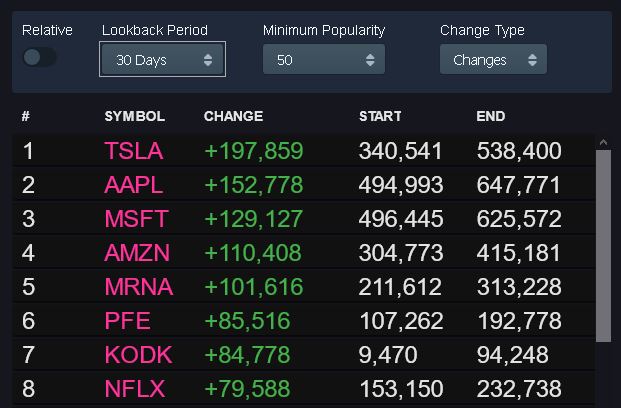

Over the past 30 days, retail investors have piled into big cap tech, with the leader being TSLA, the stock hated by most of Wall Street but loved by most of Main Street. And then you have the stocks loved by both Wall Street and Main Street: AAPL, MSFT, AMZN, MRNA, PFE, and NFLX. KODK snuck in there with a giant pump and dump move last week, which attracted daytraders like flies to turds.

Robinhood isn't a small broker that just came to the scene a few months ago, it has been around for a few years now. Yet, the huge jump in accounts holding tech stocks over the past 30 days gives you a clear view of what retail is thinking, and believing in. What they believe in is very similar to what Wall St. believes in. Big cap tech: AAPL, MSFT, AMZN, NFLX, FB. And Covid plays: MRNA, PFE, KODK? ( ;-O ) .

Reflexivity reinforces trends that have a good story with a kernel of fundamental truth: consumers and businesses going to the internet to do almost everything. That is the basis for the rush into the big cap tech names as well as SaaS/cloud stocks.

A

recent blog post by y0ungmoney goes into some detail about the big cap tech names. Especially relevant for AMZN and MSFT, as they are heavily dependent on cloud hosting for their growth, and what they are doing is charging huge subscription fees for something that can be done much more cheaply at larger firms that have the capital to hire IT workers and deploy their own servers. And GOOG and FB are much more mature companies than investors think, as online advertising is now a very big part of the advertising market, and not exactly capable of replacing TV/radio advertising which seems to be better at building brands.

And a word about the stock market now expecting a big fiscal/monetary stimulus rescue package anytime you get a slowdown in growth/recession. This goes along with the death of the business cycle that was paraded around in the late 1990s and late 2010s.

Investors are extrapolating the past 10 years into the next 10 years. That is dangerous.

1. The 10 year yield has gone from 4.0% in 2010 to 0.55% now in 2020. Unless the Fed decides to go to a -4% Fed funds rate, that kind of drop in bond yields is not happening again. So the room for monetary stimulus to benefit corporations is much less now.

2. US budget was in surplus in 2000 at the top of the business cycle. In 2018, at the top of the business cycle, US budget deficit was over $1 trillion. There is much less fiscal space to expand government spending without significant tax increases. And if there is anything we've learned, tax increases are never enough to pay for the spending. And deficits keep getting larger. But there are limits to deficit spending when it starts to erode the value of the currency. We are seeing that now as the dollar is starting to weaken as the fiscal stimulus keeps coming, doing much more than any other country in the world.

A weaker currency for a big negative trade deficit country like the US is harmful for the overall economy. The US economy is ~70% consumption, and a weaker dollar increases the price of goods which can't completely be made up for by increased exports. Eventually, the government will either have to choose between high inflation/low interest rates and low taxes or choose low inflation/higher interest rates and higher taxes.

In the long run, profligate government spending and massive deficits erode the confidence of foreigners to the US dollar, increasing the probability that it loses reserve currency status. Losing reserve currency status would instantly force the US to lower budget deficits as the demand for dollars would drastically shrink, if they don't, they could face potential Zimbabwe like inflationary pressures.

3. After tax profit margins were at an all time high in 2019, as quasi-monopolies and oligopolies became more common. There is only so much blood that capital can squeeze out of the labor rock until there is no more left. We are at the precipice of that limit with record wealth inequality. Without fatter profit margins, profit growth will be limited as growth is constrained by demographics and lack of productivity, especially now. Also corporate tax rates are historically at low levels in the US. There will be pressure to increase corporate tax rates in the coming years.

4. Workers realizing that its much easier to make money just sitting at home buying stocks receiving fat unemployment benefits than it is to go out and actually work and do something productive. And if Democrats win the 2020 election and sweep Congress, like the betting markets are forecasting, then you will get lots of government spending, and eventually universal basic income.

The US has incentivized laziness by giving away more money for those unemployed who are either daytrading at home or watching NFLX and shopping online at AMZN than to those who are working. And if working at home actually becomes more pervasive in the long run, that will decrease worker productivity, because who works harder from home than from their office? Almost no one.

5. Valuations are similar to the dotcom bubble peak for the overall market. But unlike 2000, you don't have the same growth profile and very little room to cut rates. Overvaluation is a big headwind for future returns that is underestimated by the market and its short term thinking.

Added to shorts yesterday, will add more this week as the risk/reward is very favorable.