There has been a lot of talk about the yield curve possibly inverting by the end of the year, and how that is a recession warning signal. That is confusing causation and necessity. The best recession warning signal is a falling stock market and a rising bond market. An inverted yield curve is a near necessity when the bond market almost always acts ahead of the Fed in setting interest rates.

The brief history of ZIRP/QE in the US has left very few precedents on how the yield curve reacts ahead of recession. In fact, the ZIRP era has never faced a recession in the US, since it is less than 10 years old. Thus, most fixed income analysts and prognosticators attach historical data from the pre ZIRP time period (pre 2008) to try to predict outcomes in a post ZIRP world.

The biggest difference between now and pre 2008 is financial repression, with real interest rates kept negative to induce growth and risk taking. In the past, even during recessions, real interest rates were positive, and were usually at least 2-3% during up cycles. Now, you have real interest rates that are deeply negative most of the time, and only after a long economic up cycle do they get close to zero.

So naturally, with blatant financial repression and interest rates kept too low compared to historical norms, it is harder to get a inversion of the yield curve. Yet, that is what investors are now waiting for to predict a recession. The Fed is even come out and stated that they don't want to see an inverted yield curve. How often does the Fed talk about preventing an inversion of the yield curve during boom time? Never.

In the future, it will be rare to see the yield curve invert. That is what happens when interest rates are kept too low, it makes it nearly impossible for bond investors to drive longer term yields below short term yields. Japan has been a trailblazer for what a ZIRP world will look like in the future. I recommend any fixed income investors/traders take a look at the past 40 years of JGB yield data to see how a bond market transforms when it goes from a normal interest rate market into a ZIRP market.

In Japan, the 10 year yield has been higher than the 2 year yield since 1991. The yield curve has not been inverted for 27 years. According to the so-called yield curve experts, that would mean the Japanese economy was never in danger of being in recession since 1991. Yet the Japanese economy has been at recession or near recession the whole time!

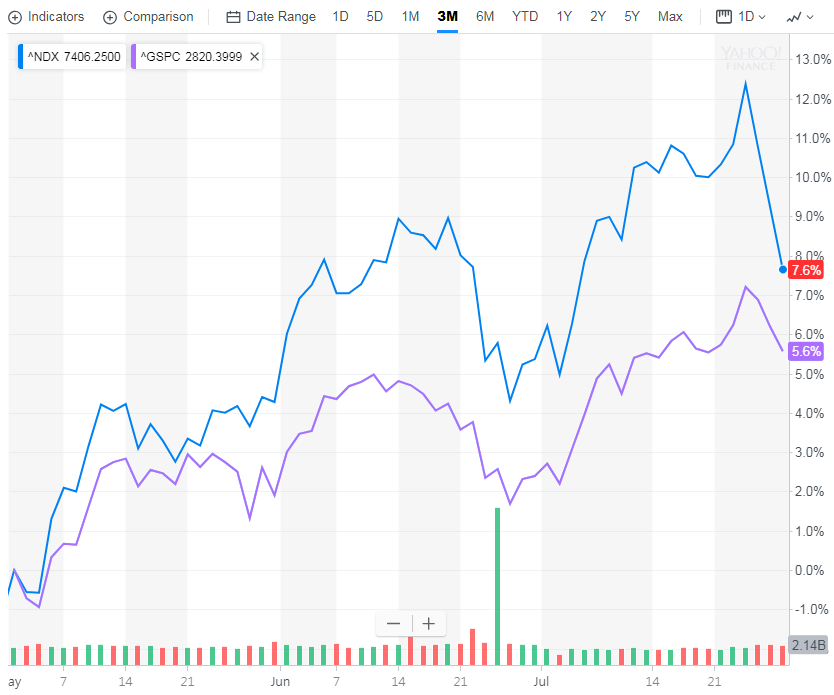

You have Powell coming to speak in front of Congress today. I expect the same tune that we heard from his past speeches, the Fed chairman usually tries to talk up the economy and show an optimistic picture on growth, labor market, and inflation. But the bond market has now calibrated its expectations to Powell towards the hawkish side, because of what he's said the last 2 Fed meetings. So it will be harder for Powell to surprise the market bearishly in the next few meetings. Thus, I expect a bullish reaction to whatever he says today, and expect the SPX to go back above 2800 later this week.