They are not getting scared. The bullishness has lasted for so long, the uptrend has gone for so long, that there is quite a bit of investor inertia. Maybe you can call it denial. But investors are not treating this selloff as something that can get really nasty, but are viewing it as a run of the mill pullback, with many viewing further downside as being limited. You are not seeing the rush towards puts as you normally see when you get a nearly 5% pullback in less than 2 weeks.

Let's compare the current selloff to the April correction. In early April, right before 3 weeks of selling in the index, you had a somewhat complacent, but not exuberant market. You didn't see rampant call buying or analysts raising their S&P 500 year end price targets left and right. You didn't hear much positive regarding the Fed, as they were still viewed to be on the sidelines, with many investors still worried about inflation.

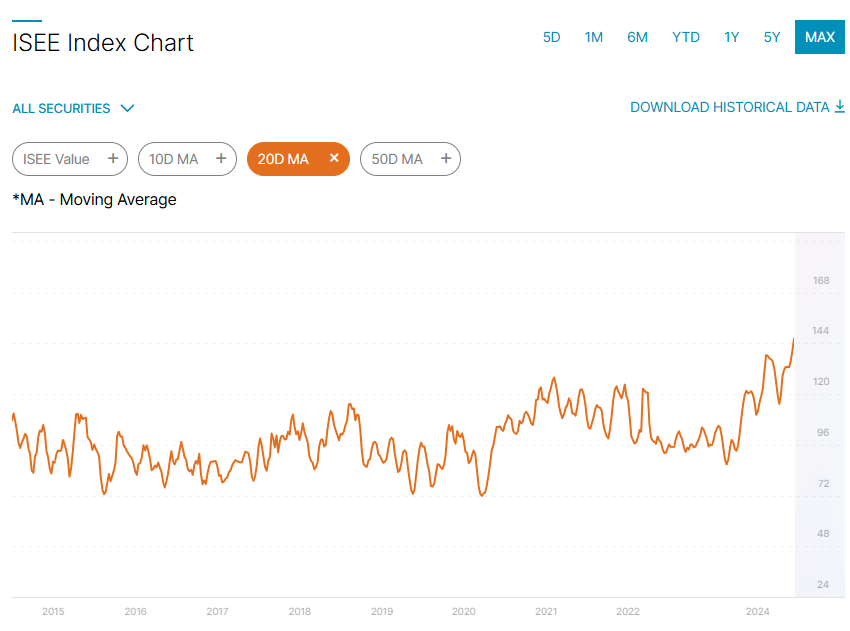

Fast forward 3 months to early July. Call buying in the Mag7 is prevalent, with lots of speculation in the big 2 options monsters, NVDA and TSLA. Inflation is now viewed as being under control, with lower than forecast CPI readings for 3 straight months. The market is now expecting and looking forward to rate cuts. They are bullish on Trump's chances of being elected, and that was viewed as a good reason to buy small caps and non Mag7 names. Breadth is expanding, which is applauded by the crowd. It is about as exuberant a market as you will see. Nearly 2021 exuberant levels. The ISEE index for the year shows the level of call buying steadily rising, reaching a peak in the first half of July. Even after a 270 point selloff in SPX, the call buying persists, and you still are not getting more puts than calls opened, which is what happened for several days during the depths of the April selloff.

The selloff in April started slowly and gained steam, as the steepest part of the selloff happened in the final week of selling, between April 15 to 19. This July selloff has been much steeper, as the rise was much steeper, with markets reacting symmetrically.

Yet, you would think that with such a steep selloff, you would get much more put buying and not so much call buying, but that's not what happened. Surprisingly, you are still seeing much more call buying than put buying here.

If you are a bull, this has to be quite concerning. You have had much more selling than in April, yet traders have not done much put buying to protect their portfolios, unlike what they did in mid April. Instead, they've been buying the dip this week and continued speculating in calls. This has added to my conviction on the short side, as this is a lot of complacency in the face of bearish and volatile price action.

The sentiment data supports this conclusion, as you are not seeing much of a drop in exposure. The NAAIM fund manager exposure index as of Thursday is still quite long despite the selling, at levels that are higher than most of 2023.

Seasonally, we are getting into negative fund flows. August is the weakest fund flow month of the year. Investors know history, and know that September and October are seasonally weak. Plus you have many on vacation and looking to de-risk ahead of the fall.

You saw more gyrations this week in investor positioning, as you got a violent unwind in the USDJPY, as the yen carry trade started to unwind. The yen carry trade is so 2007, I thought it was given up for good after the nasty rallies in the yen on past risk off moments. But with both positive carry and a steady uptrend, hedge funds have gotten greedy, and pushed their short yen exposure higher and higher. The COT data shows how lopsided the speculators are short the yen. The biggest short position in the past 10 years. I expect the yen to gain strength, regardless of the moves in the 10 year yield, as these carry traders are not trading based on yield differentials, but have just been riding a one way gravy train. With the Fed looking to cut rates starting in September, and the BOJ looking to hike rates at nearly the same time, you have a fundamental catalyst for a sharp yen appreciation. A move towards the mid 140s is definitely in the cards within the next 3 months. If that happens, that would cause even more panic selling among yen carry traders who have bought US and Japanese stocks with the proceeds of their yen borrowing.

We are seeing a big gap up today after yesterday's volatile up and down trade. I expect this gap up to fade in the first couple of hours of trade. I have a full short position, which I will look to hold for a much bigger down move. I expect this selloff to last longer than the 15 trading day selloff in April, as well as go down more than the 310 SPX points lost back then. 5250 is definitely in play in August. I will not try to predict the path to that level, but predict that it gets there within the next 3 weeks. I expect any bounces from here to be fleeting, and its not worth it to try to micro trade around the position. All the signals and indicators are lining up for nearly a perfect storm on the sell side. The setup is too bearish to play around with short term trades and potentially miss a big move.